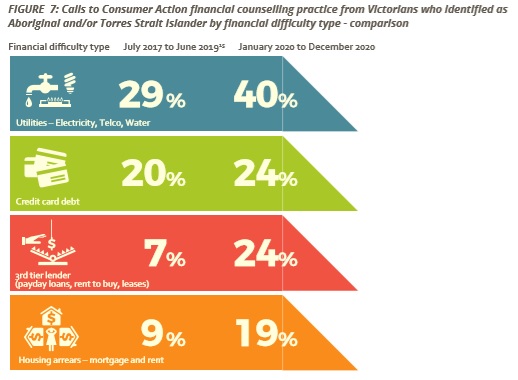

The proportion of calls made by Aboriginal Victorians to a financial counselling service to discuss problems paying their utilities bill went up by ten per cent last year, according to the service’s latest report.

Those calling to discuss problems with third tier lenders – such as pay day loans or rent to buy schemes – more than tripled from seven per cent of calls in previous years to almost 25 per cent.

Those looking for help to handle either their mortgage or rent payments went up by ten per cent.

The Consumer Action Law Centre’s report shows the effect COVID-19 and subsequent lockdowns had on Victoria’s Aboriginal community last year.

The Centre’s Integrated Practice Project – which produces the report – is now in its third year and aims to address some of the unmet consumer, credit and debt needs of Aboriginal Victorians.

The report also makes several recommendations to empower and support Victorian Aboriginal communities including better access to culturally appropriate services and making community outreach and legal education a priority for regulators, governments, and industry as we emerge from the COVID-19 crisis.

Aboriginal Policy Officer Samantha Rudolph said the report was a timely reminder that consumer issues are continuing to impact community, and will be felt in the wake of the pandemic.

“Some of the stories I’ve heard already [in 2021] are quite shocking and are unfortunately worse than the ones we have in this report released today.

That’s one of the things we’ve been trying to convey in the report: the impacts of COVID are going to be felt for years to come, and that’s why it’s so important to have not only these reports but that access to justice for people.”

Voices Heard

Now in its third year, the report focused more sharply on the stories of Aboriginal Victorians who have suffered financially from a range of issues.

A case study provided by the Victorian Aboriginal Legal Service (VALS):

“Martha was recently released from prison to a new supported residential unit. Martha needed to set up an electricity account for her new home. Martha and her VALS caseworker called several energy providers to try and get Martha connected. Each provider ran a credit check on Martha and refused to connect her because of an old utility bill. None of the providers told Martha who her Financially Responsible Market Participant (FRMP) was – essentially her ‘retailer of last resort’ that would be obliged to connect her.

Martha and her caseworker thought she might have to stay another night in prison or in a motel because they couldn’t get her electricity connected. Martha and her caseworker didn’t know that there was at least one provider who could not refuse Martha. Martha’s caseworker called the Civil Law Team at VALS to see if they could help. A civil lawyer called the Energy and Water Ombudsman (EWOV) to see if they could help. EWOV told the lawyer who the FRMP was.

Thankfully Martha was able to get her electricity connected in time to move into her new home.“

Another story, provided by the Consumer Action Law Centre, highlights the recurring issue of payday loans.

“Helen is an Aboriginal woman who called the National Debt Helpline in April 2020 seeking assistance on a number of issues. Helen called mainly asking about what to do with her multiple payday loans, and wanted to know the implications of bankruptcy.

Helen told us she is currently looking for work, and has applied for a factory job. She currently has a car on finance and is struggling to make the repayments. She has stated that she needs this car to get to this potential new factory job. She is currently living off Centrelink payments until she can secure work.

Helen told us that she currently has 4 or 5 loans to numerous lenders. Helen says this includes a loan of around $1,000 with Cash Converters, $500 with Nimble, $400 with Moneyspot, $600 with UO and a $200 loan with Cigno. Helen told us she also owes $600 to Afterpay.

Due to this, Helen is now considering bankruptcy. Helen is under 30, and for someone quite young, the impacts of bankruptcy could affect her life in the long run.

We recognised that Helen needed further support, advocacy and assessment. Helen was referred Helen to a locally based financial counsellor.

COVID Restricts Access

The onset of major lockdowns due to the COVID-19 pandemic last year hampered access for the Project team, who previously met regularly with Aboriginal communities in Victoria to discuss financial issues and raise awareness in person.

“One of the key things for us was going out to community and speaking to people first-hand,” said Ms Rudolph.

“Asking them what their experience is, what’s happening out in community and sometimes it’s hard to get that when you’re not out there.”

The full report can be viewed here.